25 Signs That Middle Class Families Are Being Wiped Out

businessinsider.com | Apr 17, 2012

by Michael Snyder

The middle class in America is being systematically wiped out, and most people don’t even realize what is happening.

The middle class in America is being systematically wiped out, and most people don’t even realize what is happening.

Every single year, millions more Americans fall out of the middle class and become dependent on the government. The United States once had the largest and most vibrant middle class in the history of the world, but now the middle class is rapidly shrinking and government dependence is at an all-time high.

So why is this happening? Well, America is becoming a poorer nation at the same time that wealth is becoming extremely concentrated at the very top. At this point, our economic system is designed to funnel as much money and power to the federal government and to the big corporations as possible. Individuals and small businesses have a really hard time thriving in this environment.

New data show grim picture of poverty

To most big corporations these days, workers are viewed as financial liabilities. Most corporations want to reduce their payrolls as much as possible. You see, the truth is that most corporations want to be just like Apple. If you can believe it, Apple makes $400,000 in profit per employee. Big corporations don’t care that you need to pay the mortgage and provide for your family. Their goal is to make as much money as possible. And most of the control freaks that run our bloated federal government don’t care much about middle class families either.

To many politicians and federal bureaucrats, middle class families are “useless eaters” that are constantly damaging the environment with their “excessive” lifestyles. In this day and age, neither the federal government nor the big corporations really have much use for middle class Americans, and that is really, really bad news for the the future of the middle class family in America.

There are three key factors that are constantly chipping away at the middle class….

-Globalization

-Inflation

-Taxes

Labor has become a global commodity, and American workers are often 10 to 20 times as expensive as workers on the other side of the world are. Middle class jobs (such as manufacturing, etc.) have been leaving this country at an astounding pace. Competition for the jobs that remain has become extremely fierce, and this has driven wages down. The following is from a recent article in the New York Times….

But in the last two decades, something more fundamental has changed, economists say. Midwage jobs started disappearing. Particularly among Americans without college degrees, today’s new jobs are disproportionately in service occupations — at restaurants or call centers, or as hospital attendants or temporary workers — that offer fewer opportunities for reaching the middle class.

As paychecks have stagnated, the cost of living has continued to escalate. Middle class families are finding that their paychecks simply do not go nearly as far as they did before. This is creating a tremendous amount of financial stress in households all over America.

Meanwhile, our politicians are taxing the middle class like crazy. Most people only focus on federal and state income taxes, but that is only a small part of the story. As I detailed the other day, our politicians are taxing us in literally dozens of different ways and it is almost always the middle class that ends up getting hit the hardest.

If America wants to be great again, it is going to need a thriving middle class. But right now the federal government and the big corporations are gobbling up all of the power and all of the money and the middle class is shrinking rapidly.

If current trends continue, eventually there will not be much of a middle class left.

The following are 25 signs that middle class families have been targeted for extinction….

#1 Over the past several decades, millions upon millions of middle class Americans have been systematically turned into government dependents. Back in 1960, social welfare benefits made up approximately 10 percent of all salaries and wages. In the year 2000, social welfare benefits made up approximately 21 percent of all salaries and wages. Today, social welfare benefits make up approximately 35 percent of all salaries and wages.

#2 Unemployment is at epidemic levels and the vast majority of the new jobs that have been “created” in recent years have been low paying jobs. Of those Americans that do have a job at this point, one out of every four works a job that pays $10 an hour or less.

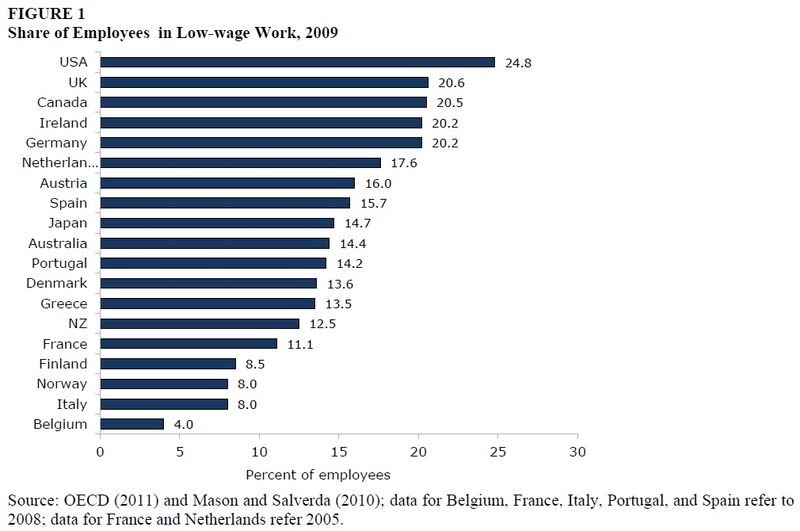

#3 The “working poor” is a group that is rapidly growing in this country. If you can believe it, the United States actually has a higher percentage of workers doing low wage work than any other major industrialized nation does.

#4 Over the past several decades, the percentage of low income jobs has steadily increased. Back in 1980, less than 30% of all jobs in the United States were low income jobs. Today, more than 40% of all jobs in the United States are low income jobs.

#5 The way that our economic system is structured today, almost all of the economic rewards go to the very top of the food chain. The following is how income gains in the United States were distributed during 2010….

-37 percent of all income gains went to the top 0.01 percent of all income earners

-56 percent of all income gains went to the rest of the top 1 percent

-7 percent of all income gains went to the bottom 99 percent

#6 Several decades ago, there was a much more even distribution of income in this country. Back in the 1970s, the top 1 percent of all income earners brought in about 8 percent of all income. Today, they bring in about 21 percent of all income.

#7 As the middle class shrinks, the number of “low income” and “poor” Americans is rapidly rising. Today, approximately 48 percent of all Americans are currently either considered to be “low income” or are living in poverty.

#8 Manufacturing jobs once enabled huge numbers of Americans to enjoy a middle class lifestyle. Unfortunately, those jobs are leaving this country at a breathtaking pace. Back in 1940, 23.4% of all American workers had manufacturing jobs. Today, only 10.4% of all American workers have manufacturing jobs.

#9 In the old days, any man that was willing to work hard and wanted a job could get one. Today, there are millions of American men sitting on their couches at home wondering why nobody will hire them. Back in 1950, more than 80 percent of all men in the United States had jobs. Today, less than 65 percent of all men in the United States have jobs.

#10 The middle class is shrinking at the same time that America is getting poorer as a nation. In the middle of the last century, the United States was #1 in the world in GDP per capita. Today, the United States is #13 in GDP per capita.

#11 Every year now, we see millions of Americans fall out of the middle class. In 2010, 2.6 million more Americans descended into poverty. That was the largest increase that we have seen since the U.S. government began keeping statistics on this back in 1959.

#12 The shrinking middle class is having a disproportionate impact on children. At this point, approximately 22 percent of all American children are living in poverty.

#13 In the old days, most Americans grew up in middle class neighborhoods. Sadly, this is no longer true. In 1970, 65 percent of all Americans lived in “middle class neighborhoods”. By 2007, only 44 percent of all Americans lived in “middle class neighborhoods”.

#14 The concentration of wealth at the very top of the food chain is astounding. Right now, over 50 percent of all stocks and bonds are owned by just 1 percent of the U.S. population.

#15 When you concentrate too much power in the hands of the federal government and the big corporations, it is inevitable that massive amounts of wealth will become concentrated in just a few hands. In the United States today, the wealthiest one percent of all Americans have a greater net worth than the bottom 90 percent combined.

#16 There is nothing wrong with making money, but there is something wrong with a game where individuals and small businesses cannot compete fairly. According to Forbes, the 400 wealthiest Americans now have more wealth than the bottom 150 million Americans combined.

#17 When the number of poor people rapidly expands in a society, that is a recipe for social unrest. At this point, the poorest 50 percent of all Americans collectively own just 2.5% of all the wealth in the United States.

#18 The hidden tax of inflation is absolutely devastating middle class families all over America. Since 1970, the U.S. dollar has lost more than 83 percent of its value. Any dollars that middle class families try to save are constantly losing a little bit more value every single day.

#19 American workers that try to play by the rules find that they are constantly fighting a losing battle. According to one study, between 1969 and 2009 the median wages earned by American men between the ages of 30 and 50 dropped by 27 percent after you account for inflation.

#20 In recent years, many middle class families have seen their paychecks get smaller. Median household income in the United States has fallen 7.8 percent since December 2007 after adjusting for inflation.

#21 In recent years, many middle class families have seen many of their basic expenses absolutely soar. For example, health insurance costs have risen by 23 percent since Barack Obama became president.

#22 Just turning on the lights and heating their homes has become a major burden for many middle class families. Electricity bills in the United States have risen faster than the overall rate of inflation for five years in a row.

#23 Just putting gas in the car has become a major financial ordeal for millions of hard working Americans. The average price of a gallon of gasoline in the United States has increased by more than 100 percent since Barack Obama became president.

#24 Sadly, government dependence is now at an all-time high, and that is the way that many among the elite like it. When Barack Obama took office, there were 32 million Americans on food stamps. Now, there are more than 46 million Americans on food stamps. In particular, an astounding number of children are on food stamps right now. At this point, approximately one-fourth of all American children are enrolled in the food stamp program.

#25 Many middle class families will not be in the middle class for too much longer. According to a shocking new study from the National Bureau of Economic Research, 200,000 U.S. households will use the money from their tax refunds this year “to pay for bankruptcy filing and legal fees“.

Unless major changes are made on a national level, the middle class is going to continue to disappear.

If you are playing the game the way that the system tells you to play it and you expect to live a middle class lifestyle for many years to come there is a good chance that you will be deeply disappointed at some point.

Millions upon millions of Americans have done everything that the system told them to do and the system has still failed them. They got good grades all the way through school, they went to college, they worked really hard, they stayed out of trouble and they gave everything they could to their employers. In spite of all that, millions of hard working families have still lost their jobs and their homes in recent years.

Do not trust that the system will take care of you, and you should not trust that the government will take care of you either.

We don’t need the federal government to hand out more money to everyone. Government handouts are already at record levels and the government is not even coming close to paying for all of this reckless spending.

More government spending is not going to solve any of our problems.

Instead, what we need is an environment where the size and power of the federal government is limited and the size and the power of the big corporations is limited. We need an environment where individuals and small businesses can thrive and compete fairly.

Unfortunately, neither major political party is going to move us in that direction, so there is not much hope for solutions on the national level any time soon.

On an individual level, we can all learn how to prepare for the very difficult years that are coming. It is imperative that we all work to become more independent of the system, because the system could fail at any time.

If you have blind faith that your job will always be there and that the federal government will rescue you if the economy crashes then you are likely to be bitterly disappointed at some point.

The truth is that our economy is slowly dying and the great American middle class is being systematically wiped out.

Many of the things that worked in the past are not going to work any longer.

You can choose to adapt or you can suffer the consequences.

Our world is rapidly changing, and we all need to prepare for what is coming.

{kind=link}

{kind=link}